You can use a personal loan for home improvement if you want a lump sum of cash to fund renovations without using your house as collateral. These are typically unsecured, meaning you aren’t putting your property at risk to get the money you need for upgrades.

Unsecured Loans vs. Tapping Your Equity

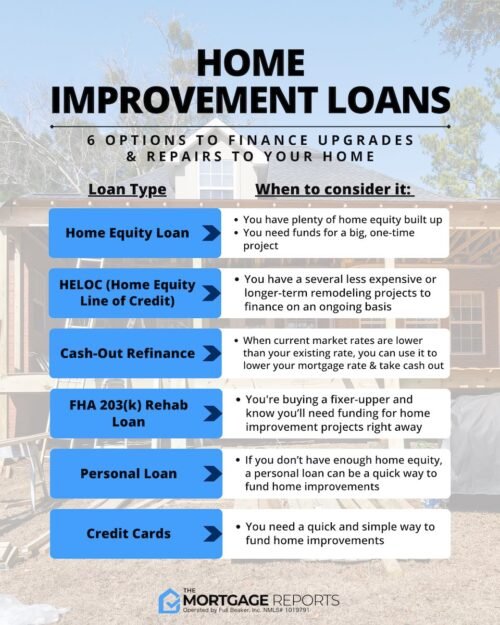

When you decide it is finally time to tear out those 1990s laminate countertops and replace them with something that doesn’t look like a relic, you face a fork in the road. You can borrow against the value of your home, which is what people do when they take out a Home Equity Line of Credit (HELOC) or a home equity loan. But there is a catch: those methods involve your house as collateral. If things go south, the bank could technically come for the roof over your head.

Personal loans for home improvements offer a way around that anxiety. Because they are unsecured, you don’t put your house up as collateral, which makes the application process much faster and less invasive. You aren’t dealing with a lengthy appraisal or the legal headache of a new mortgage lien. It is a cleaner, albeit sometimes more expensive, way to get the job done.

But don’t mistake “easier” for “free money.” Since the lender isn’t holding your home as a guarantee, they care much more about your credit score and your monthly income. If your credit is pristine, you might find the interest rates quite palatable. If it’s a bit bruised, you might pay a premium for that convenience. It is a trade-off between the security of your asset and the speed of your renovation project.

I’ve seen people spend months agonizing over whether to refinance their mortgage just to get an extra $20,000 for a bathroom remodel, only to realize that a simple personal loan would have solved the problem in a week. It is about matching the tool to the task. If you are doing a massive, whole-house structural overhaul, equity might make sense. If you are just fixing a leaky roof or upgrading the plumbing, a personal loan is often the smarter, faster path.

What Exactly Can You Buy With the Cash?

One of the biggest misconceptions is that you need a specific “home improvement” product that comes with a list of approved contractors or restricted spending rules. That isn’t usually how it works. Once that lump sum hits your bank account, it is your money. You aren’t tied to a specific hardware store or a single plumber, which gives you more leverage when negotiating with contractors.

According to Wells Fargo’s guide to home improvement personal loans, you can use these funds for a wide variety of needs. You might decide to remodel a specific room, like a kitchen or a basement. You could use it to cover essential home repairs that you simply can’t afford to wait on, or you might even want to make a new addition, like a sunroom or a finished garage space. There is even an option to plan for green energy upgrades, such as solar panels or high-efficiency HVAC systems, which can save you money on utility bills in the long run.

This flexibility is a big advantage. If you find a great deal on a high-end refrigerator or a set of custom cabinets, you can pull the trigger immediately. You don’t have to submit receipts to a bank to prove you actually bought the items you said you would. This liquidity is why many homeowners prefer this method for “mid-range” projects, the things that aren’t life-threatening emergencies but are definitely not optional for a comfortable life.

It is a strange sensation to have thousands of dollars sit in your checking account, knowing it is earmarked for a new deck but technically available for anything. You have to be disciplined. It is easy to see a new car or a luxury vacation in the periphery of your budget when you have that sudden influx of cash. Stay focused on the project, or the “home improvement” loan quickly becomes a “lifestyle upgrade” loan.

Comparing Your Financing Options

You might find yourself staring at a dozen different websites, all claiming to have the best rates for 2026. It gets overwhelming quickly. To make sense of it, you need to look at the actual structure of the debt. Most of these are lump-sum, fixed-rate loans that you will repay in monthly installments over a set period. This predictability is helpful because you know exactly what your monthly outflow will be from month one until the debt is gone.

If you are looking for specifics, it helps to categorize your needs. Are you looking for a quick fix or a long-term investment? If you need money quickly for smaller projects or emergencies, such as a new roof or upgraded plumbing, some lenders specialize in these quick-turnaround needs. You can check out how different lenders approach these scenarios through providers like Navy Federal Credit Union to see how their terms compare to traditional big banks.

Here is how the primary players generally stack up:

| Feature | Unsecured Personal Loan | Home Equity Loan/HELOC |

|---|---|---|

| Collateral | None (Unsecured) | Your Home (Secured) |

| Approval Speed | Very Fast (Days) | Slow (Weeks/Months) |

| Interest Rates | Generally Higher | Generally Lower |

| Impact on Credit | Minimal (unless defaulted) | Can affect mortgageability |

The numbers matter more than the marketing. A lower interest rate sounds great on a brochure, but if the closing costs and appraisal fees associated with a home equity loan eat up the first two years of your savings, the “cheap” loan becomes expensive. Conversely, a high-interest personal loan might be “expensive” on paper, but if it allows you to finish a kitchen renovation before the holidays, the value it adds to your life might outweigh the extra interest paid. You have to weigh the math against your personal timeline and your tolerance for risk.

And remember, your credit score is the primary driver here. If you are looking at a site like texasloanstoday.com or other comparison tools, you’ll notice that the rates offered are often “starting at” certain percentages. Those lowest rates are reserved for people with exceptional credit. If your score is in the mid-600s, prepare to see those numbers climb significantly.

The Hidden Logic of Interest Rates

People often ask why they shouldn’t just use a credit card for a small renovation. If you are buying a $500 faucet, use the card. If you are replacing the entire HVAC system, a credit card is a financial trap. The interest rates on cards are significantly higher than even the most expensive personal loan, and the “pay monthly” trap can lead to years of debt for a project that should have been settled in a single season.

But wait, there is a catch to the “fixed-rate” promise. While your monthly payment stays the same, the total amount of interest you pay is heavily dependent on the term length. If you take a five-year loan instead of a three-year loan, your monthly payment is much lower and easier to manage, but you will end up paying hundreds, even thousands, more in interest over the life of the loan. It is a classic case of “cheap monthly, expensive total.”

I’ve talked to homeowners who were so relieved by the low monthly payment on their renovation loan that they didn’t realize they were essentially paying for their new granite countertops three times over by the time they finished the term. You need to look at the “Total Cost of Borrowing.” It is a simple calculation: (Monthly Payment x Number of Months) – Principal Amount. That number tells you the real price of your renovation.

If you are planning a project that will increase your home’s value, such as a bathroom remodel or an addition, you should try to time the loan so that the project is finished and the value is realized before you need to refinance your primary mortgage. A well-executed renovation can be a tool for wealth building, but only if the cost of the debt doesn’t outpace the equity gained.

The “What If” Factor: Addressing the Skeptic

You might be thinking, “Why would I take on any more debt when interest rates are already a mess?” It is a fair question. If you can afford the project out of pocket, you should. Debt is a tool, and like any tool, it can be used to build something beautiful or to cause a lot of damage. The skepticism is healthy. You should be skeptical of any loan that doesn’t clearly outline its terms, fees, and the consequences of a missed payment.

However, the real question isn’t whether you should take a loan, but whether the specific project justifies the specific loan. If the renovation is purely aesthetic, like painting a room a trendy color, don’t touch a loan. If the renovation is functional, like a leaking roof or an outdated electrical system that poses a fire hazard, the loan is an investment in your safety and the long-term viability of your most expensive asset. If you use the money to fix things that work, you aren’t just spending; you are preserving.

Good to know

Should I use a personal loan or a home equity loan for home improvements?

Personal loans offer faster funding and fixed rates without using your home as collateral, while home equity loans typically provide lower interest rates and larger sums for major renovations.

Can I use a personal loan for home remodeling?

Yes, personal loans are unsecured funds that can be used for any legitimate home improvement project, from small repairs to large-scale renovations.

Will a personal loan for home improvement affect my credit score?

Applying for a loan involves a hard inquiry which may cause a temporary dip in your score, but consistent on-time repayments can help improve it over time.

What is the difference between a personal loan and a HELOC for renovations?

A personal loan provides a lump sum with fixed terms, whereas a Home Equity Line of Credit (HELOC) works like a credit card with variable rates and flexible access to funds.

Are personal loans better than credit cards for home repairs?

Personal loans are generally better for large repairs because they offer lower interest rates and fixed monthly payments compared to the high, variable interest of credit cards.